-

Why My Best Backtest Almost Cost Me Real Money in Live Trading

The $55,000 Backtest That Wasn’t Real The reality of backtest vs live trading is that the two often produce different numbers. The first time I ran a serious backtest on a strategy I was developing, the equity curve came back showing fifty-five thousand dollars of profit over ten years on a starting balance of six…

-

Why I Run Two Different VPS Providers for Forex and Crypto (And What I Learned)

The Setup Behind the Live Signal I run a live MT5 EA on USDJPY one-hour bars from a VPS in New York, and three separate crypto futures bots on Binance, Bitget, and Bybit from a different VPS in Tokyo. The total cost of both VPS combined is about eighteen dollars a month. That number surprises…

-

How I Connected Python to MT5 to Run a Real Live Trading Signal (And What Broke)

The Promise That Sold Me on Connecting Python to MT5 I started this project because I wanted to do something that sounded simple. I wanted my Python analytics to send a real signal to MetaTrader 5 and let MT5 actually place the order on my broker. Not a paper trade. Not a simulated fill. A…

-

What I Learned Running Live Bots on Binance, Bybit, and Bitget: 7 Production Bugs and Their Fixes

Three Exchanges, 7 Bugs, One Year of Lessons For the past year I have run live trading bots simultaneously on Binance Futures, Bybit USDT-M perpetuals, and Bitget USDT-FUTURES. Three exchanges, three different APIs, three slightly different mental models of what an order even is. The strategies were similar across all three. The execution layers were…

-

How to Connect TradingView Webhooks to Python for Automated Trading: A Production Guide

The Bridge I Wish Someone Had Drawn for Me Seven Years Ago The first time I tried to connect a TradingView webhook to a live Python execution layer, I was running small accounts across Bybit, Binance, and Bitget from a laptop. The signal fired at 3:47 AM on a Tuesday. My laptop had gone to…

-

Escaping the CEX Trap: Architecting a Python Arbitrage Engine for Decentralized Exchanges (DEX) and On-Chain Liquidity

The Closed System and Its Limits Every architectural pillar constructed across this series has operated within a single conceptual perimeter: the centralized exchange. Binance, Bybit, Bitget, OKX, KuCoin. The microstructure analytics consume their order books. The reinforcement learning agent allocates across their spot and perpetual markets. The sentiment engine scores news that moves their tickers.…

-

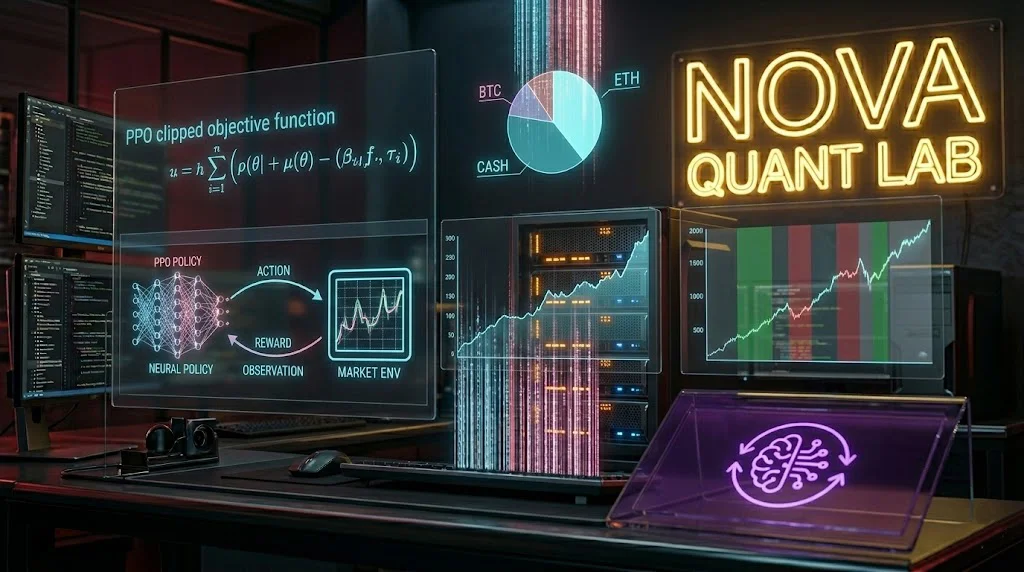

The Next Frontier: Integrating Deep Reinforcement Learning (PPO) for Dynamic Portfolio Allocation in Python

The Structural Ceiling of Supervised Learning Every machine learning architecture deployed across this series so far has shared a common epistemic foundation. The LightGBM ensemble for high-frequency arbitrage, the LSTM sequential model for pattern recognition, the meta-model stacked on top of both, and the purged k-fold cross-validation framework that validated them all. Each of these…

-

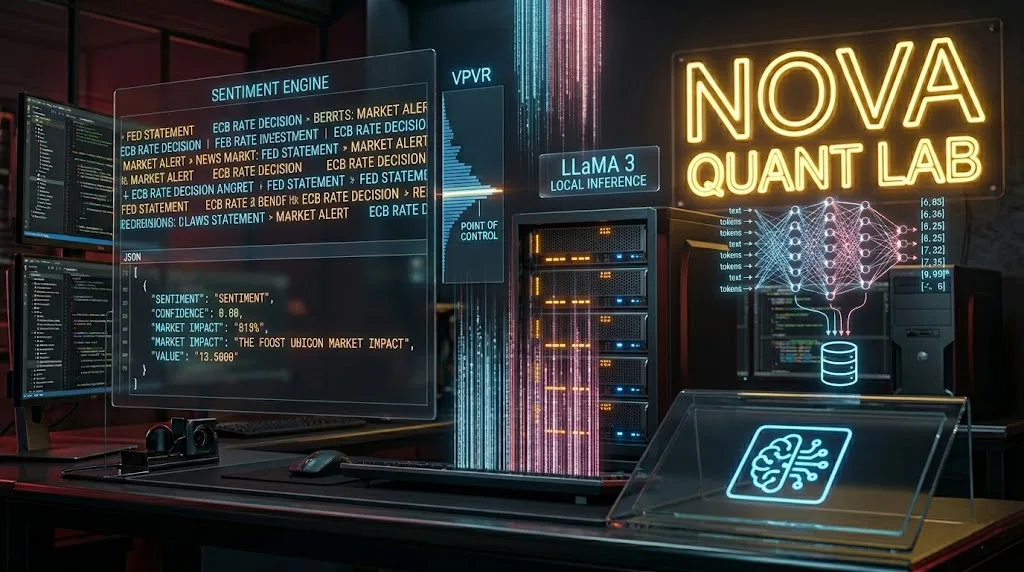

The Sentiment Engine: Deploying Local LLMs (LLaMA 3) for Real-Time Macroeconomic and News Sentiment Analysis in Algorithmic Trading

The Latency Tax of Cloud-Hosted LLM APIs The analytical surface constructed across this series has been deliberately quantitative. Order flow toxicity, volume profile acceptance, microstructure imbalance, columnar tick storage. Each pillar has dealt exclusively with numerical signals derived from market data itself. There is, however, an entirely separate information channel that moves the same markets…

-

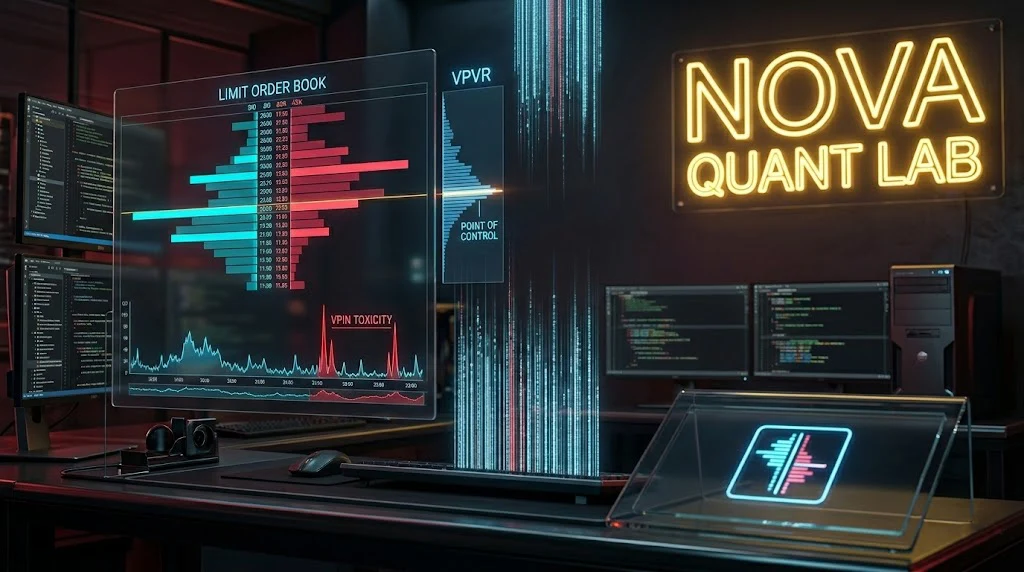

Order Flow Toxicity and Microstructure: Detecting Institutional Accumulation using VPVR and Order Book Imbalance in Python

The Blind Spot of Price-Only Models Every strategy constructed up to this point in the series, from the LightGBM arbitrage engine to the LSTM sequential model and the reinforcement learning portfolio allocator, has shared one common input surface: price and its derivatives. Returns, volatility, moving averages, Fibonacci projections, Elliott wave counts, cointegration residuals. All of…

-

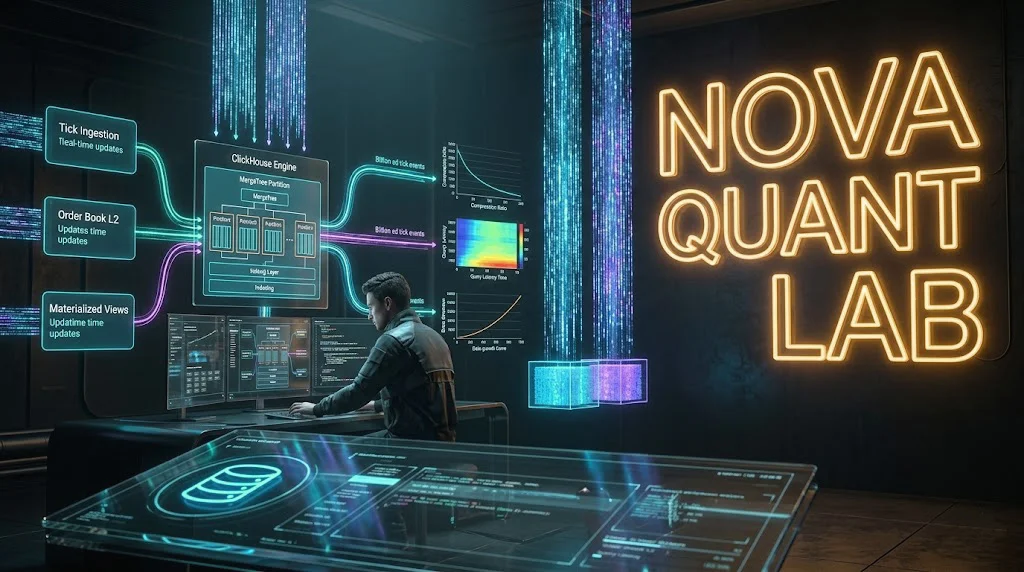

The Quant Fund Architecture: Designing an Institutional-Grade Data Warehouse with ClickHouse and Python for Tick-Level Analytics

The Structural Failure of Row-Based Storage at Tick Resolution The custom PostgreSQL pipeline constructed earlier in this series was engineered to replace Myfxbook’s opaque verification layer and stream MT5 plus CCXT metrics through a secured FastAPI backend. For trade-level tracking of a curated fleet, that architecture holds. Its load-bearing capacity is more than adequate when…