Category: Python Trading

-

How I Connected Python to MT5 to Run a Real Live Trading Signal (And What Broke)

The Promise That Sold Me on Connecting Python to MT5 I started this project because I wanted to do something that sounded simple. I wanted my Python analytics to send a real signal to MetaTrader 5 and let MT5 actually place the order on my broker. Not a paper trade. Not a simulated fill. A…

-

Escaping the CEX Trap: Architecting a Python Arbitrage Engine for Decentralized Exchanges (DEX) and On-Chain Liquidity

The Closed System and Its Limits Every architectural pillar constructed across this series has operated within a single conceptual perimeter: the centralized exchange. Binance, Bybit, Bitget, OKX, KuCoin. The microstructure analytics consume their order books. The reinforcement learning agent allocates across their spot and perpetual markets. The sentiment engine scores news that moves their tickers.…

-

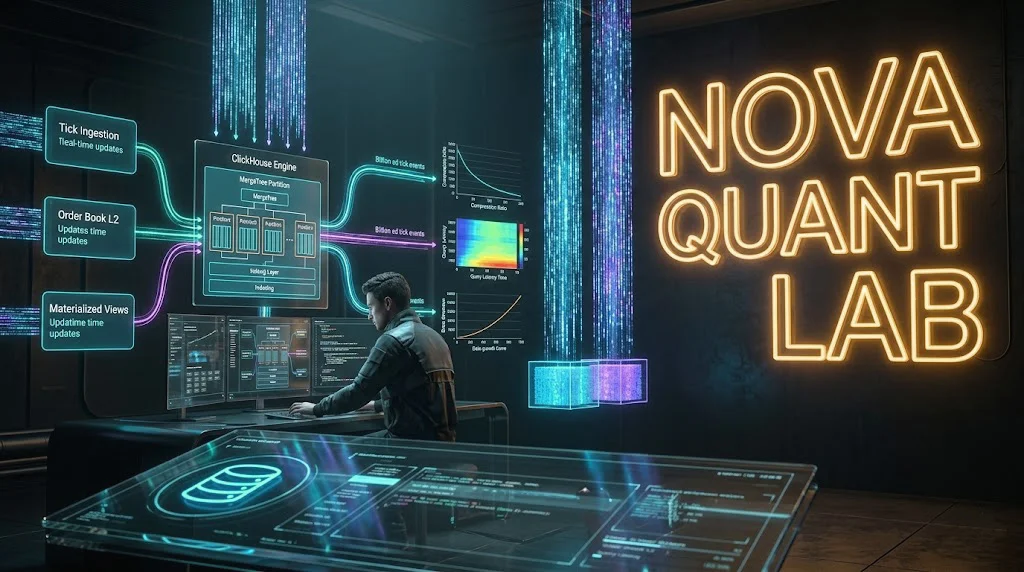

The Quant Fund Architecture: Designing an Institutional-Grade Data Warehouse with ClickHouse and Python for Tick-Level Analytics

The Structural Failure of Row-Based Storage at Tick Resolution The custom PostgreSQL pipeline constructed earlier in this series was engineered to replace Myfxbook’s opaque verification layer and stream MT5 plus CCXT metrics through a secured FastAPI backend. For trade-level tracking of a curated fleet, that architecture holds. Its load-bearing capacity is more than adequate when…

-

Customizing the VNPY BacktestingEngine: A Deep Dive into Institutional Strategy Architecture

The quantitative trading community often treats backtesting engines as “truth machines.” You feed in historical data, apply a logic, and the engine spits out an equity curve. For the majority of retail traders, open-source frameworks like VNPY are seen as plug-and-play solutions. They trust the default matching logic, they apply a fixed slippage value, and…

-

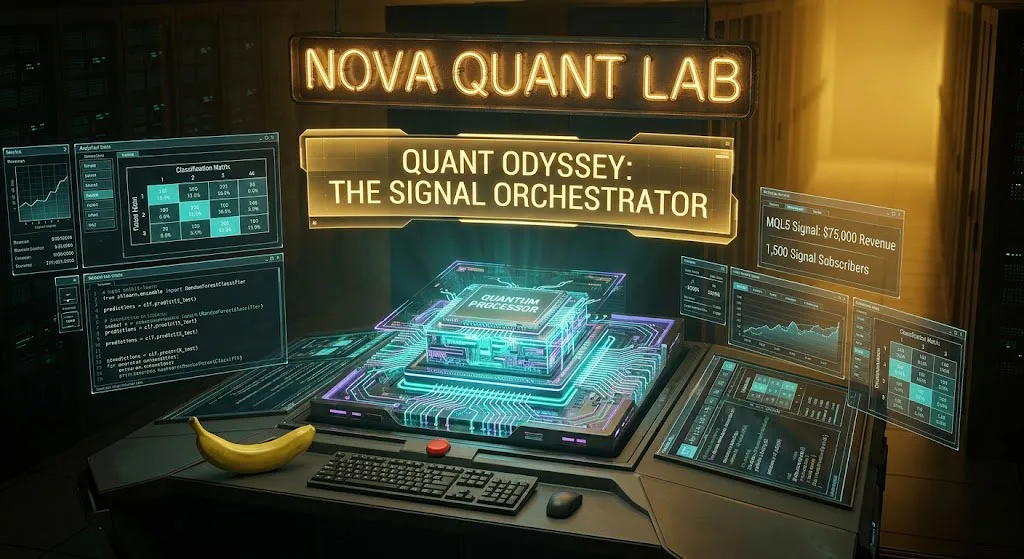

The Brain of the Machine: Designing a High-Precision Net-Yield Signal Orchestrator in Python

Welcome back to Nova Quant Lab. We have reached the pivotal milestone in our Season 2 journey. Over the last few weeks, we have successfully engineered the sensory organs (the Asynchronous Data Ingestion Module) and the muscular system (the Concurrent Execution Engine) of our algorithmic trading bot. Our server is now flooded with real-time, Level…

-

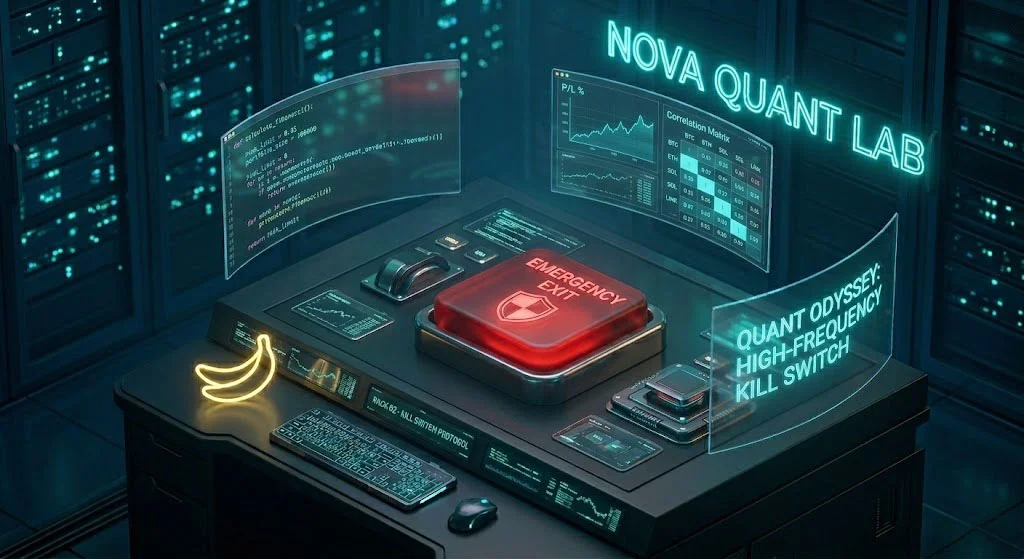

The Unbreakable Grip: Designing a Risk-Managed Asynchronous Execution Engine in Python

Welcome back to Nova Quant Lab. In our previous session, we successfully engineered the central nervous system of our arbitrage bot: The Asynchronous Data Ingestion Module. Using the robust ccxt.pro library and Python’s asyncio loop, we established persistent, always-on WebSocket connections that stream Level 2 Order Books from the Binance matching engine with near-zero latency.…

-

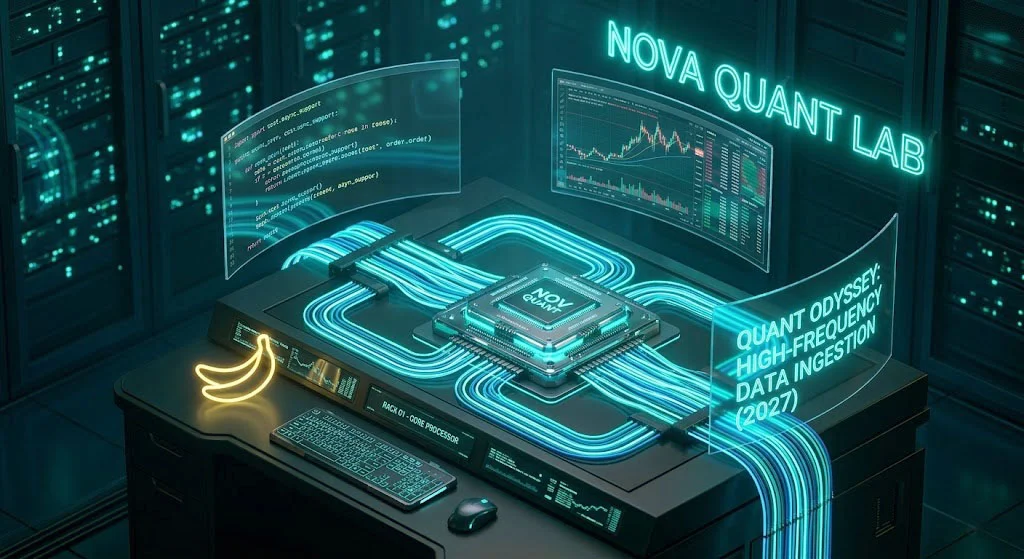

Building the Engine: Asynchronous Real-Time Order Book Ingestion with Python and CCXT

Welcome back to Nova Quant Lab. In our previous post, we fundamentally shifted our trading philosophy. We abandoned the emotional, unpredictable game of directional guessing and embraced the mathematical certainty of Delta-Neutral Arbitrage. We established that by holding opposing positions across the Spot and Perpetual Futures markets, we can eliminate market risk and harvest the…

-

Algorithmic Approach to Elliott Wave Theory: Building Momentum Indicators (2026 Guide)

Welcome back to Nova Quant Lab. In our previous session, we successfully engineered a Python algorithm to detect structural market swings and calculate dynamic Fibonacci retracement zones. We transitioned from reacting to lagging indicators to anticipating price action at mathematically proven levels of structural support. Today, we are tackling what is arguably the most complex,…

-

Coding Fibonacci Retracements and Price Action Signals in Python (2026 Advanced Guide)

Welcome back to Nova Quant Lab. Over our last two sessions, we stepped away from pure quantitative analysis to build out our professional infrastructure. We successfully deployed a fleet of independent trading bots onto a 24/7 Virtual Private Server (VPS) and implemented centralized logging with advanced batch script automation. Our structural foundation is now rock…

-

Mastering Data Visualization for Quants: Plotting Equity Curves and Drawdowns with Python (2026)

Welcome to the next critical installment of the Nova Quant Lab engineering series. In our previous deep dives, we constructed a comprehensive technical infrastructure, ranging from secure Binance API integration to the rigorous mathematical validation of Backtesting 101. However, the true test of a quantitative developer lies not merely in the generation of trade signals,…