-

The Brain of the Machine: Designing a High-Precision Net-Yield Signal Orchestrator in Python

Welcome back to Nova Quant Lab. We have reached the pivotal milestone in our Season 2 journey. Over the last few weeks, we have successfully engineered the sensory organs (the Asynchronous Data Ingestion Module) and the muscular system (the Concurrent Execution Engine) of our algorithmic trading bot. Our server is now flooded with real-time, Level…

-

The Unbreakable Grip: Designing a Risk-Managed Asynchronous Execution Engine in Python

Welcome back to Nova Quant Lab. In our previous session, we successfully engineered the central nervous system of our arbitrage bot: The Asynchronous Data Ingestion Module. Using the robust ccxt.pro library and Python’s asyncio loop, we established persistent, always-on WebSocket connections that stream Level 2 Order Books from the Binance matching engine with near-zero latency.…

-

Building the Engine: Asynchronous Real-Time Order Book Ingestion with Python and CCXT

Welcome back to Nova Quant Lab. In our previous post, we fundamentally shifted our trading philosophy. We abandoned the emotional, unpredictable game of directional guessing and embraced the mathematical certainty of Delta-Neutral Arbitrage. We established that by holding opposing positions across the Spot and Perpetual Futures markets, we can eliminate market risk and harvest the…

-

The End of Directional Guessing: How to Build a “Risk-Free” Crypto Arbitrage Bot in Python

Welcome to Season 2 of Nova Quant Lab. In Season 1, we focused heavily on building the technical foundation. We covered Python environments, MT5 integration, setting up 24GB cloud servers, and connecting to global exchange APIs. We built the infrastructure. But I haven’t fully shared why I became so obsessed with algorithmic trading in the…

-

Monetizing Your Python Trading Algorithms: The Ultimate Guide to the MQL5 Market (2026)

Welcome to the pinnacle of Nova Quant Lab. Over our past 19 sessions, we have embarked on an extraordinary engineering journey. We started with basic API connections and scaled into a fully automated, asynchronous 5-node arbitrage fleet running 24/7 on a Linux Virtual Private Server. We secured our structural integrity with advanced fractional risk management…

-

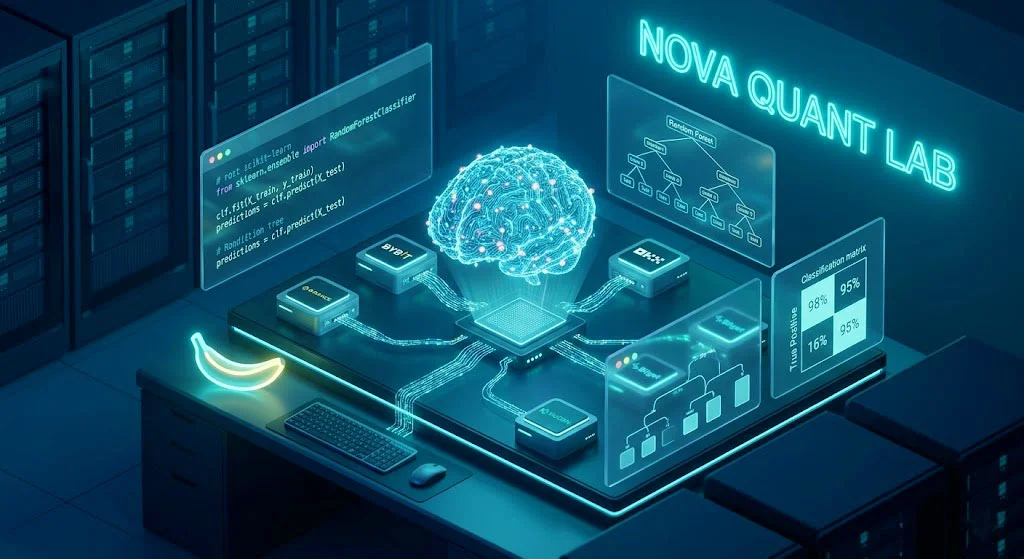

Introduction to Machine Learning for Crypto Market Prediction: Scikit-learn Tutorial (2026 Guide)

Welcome back to Nova Quant Lab. Over our previous 18 sessions, we have successfully engineered a monolithic, high-performance quantitative architecture. We established a 5-node asynchronous execution fleet spanning Binance, Bybit, OKX, Bitget, and KuCoin. We fortified this infrastructure with dynamic fractional risk sizing, and we subjected our final outputs to rigorous, unalterable third-party auditing via…

-

Integrating Myfxbook API to Verify Your 5-Node Algorithmic Fleet and Trading Results (2026 Guide)

Welcome back to Nova Quant Lab. Over our last 17 sessions, we have engineered a highly sophisticated, fully automated quantitative trading infrastructure. We have deployed our Python algorithms on a 24/7 Virtual Private Server (VPS), implemented asynchronous multi-exchange arbitrage across five major global exchanges, and secured our structural integrity with dynamic Fractional Risk sizing and…

-

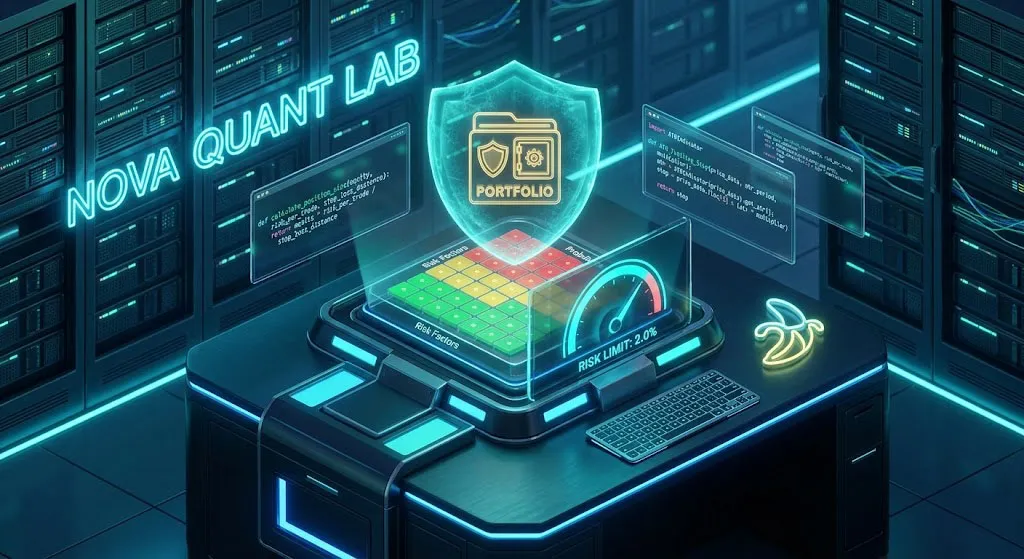

Advanced Risk Management: Dynamic Position Sizing & Trailing Stops in Python (2026 Guide)

Welcome back to Nova Quant Lab. Over our last 16 sessions, we have engineered an incredibly aggressive, high-performance quantitative infrastructure. We have deployed asynchronous multi-exchange arbitrage bots, bridged Python with MetaTrader 5, and translated subjective Elliott Wave momentum into objective algorithmic triggers. However, all of that offensive capability is mathematically irrelevant if you ignore the…

-

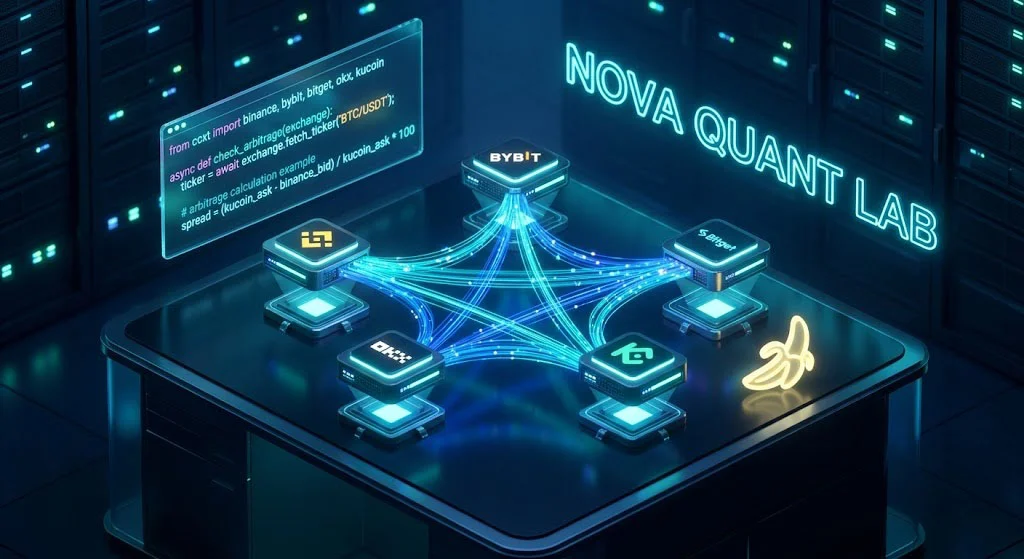

Multi-Exchange Arbitrage: Connecting Binance, Bybit, OKX, Bitget, and KuCoin via Python (2026 Advanced Guide)

Welcome back to Nova Quant Lab. Over our last 15 sessions, we have constructed a formidable, professional-grade quantitative trading infrastructure. We deployed our algorithms on a 24/7 Virtual Private Server (VPS), modularized our strategies to eliminate single points of failure, and bridged the gap between Python’s analytical processing power and institutional execution speeds. Now, we…

-

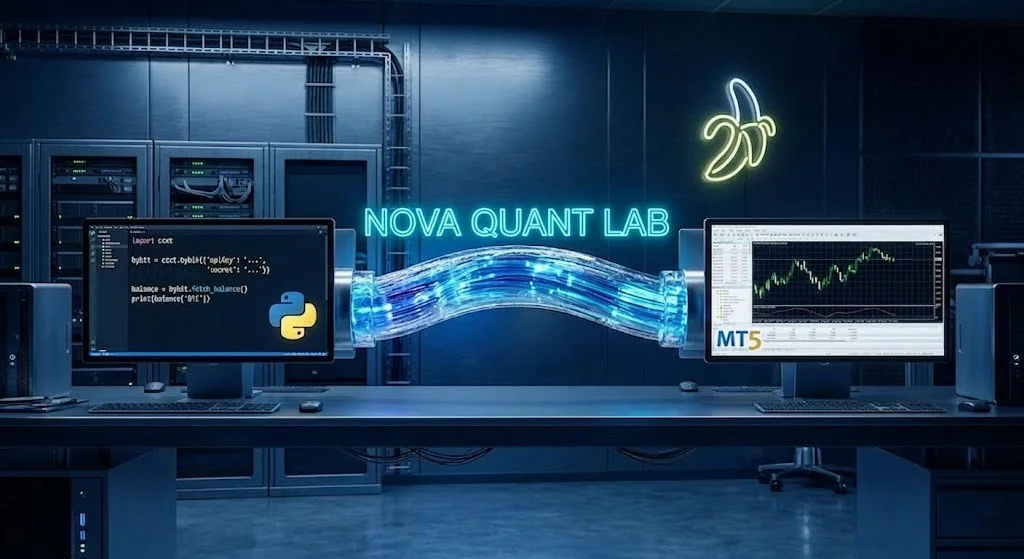

Python vs. MQL5: Bridging the Gap for Advanced Algorithmic Trading (2026 Guide)

Welcome back to Nova Quant Lab. Over our previous sessions, we have established a highly resilient, 24/7 automated trading infrastructure on a VPS. We have engineered Python algorithms to detect Fibonacci retracements and objectively quantify Elliott Wave momentum divergences. Our structural foundation is robust, and our analytical logic is precise. Up until this point, our…