Category: Algorithmic Trading

-

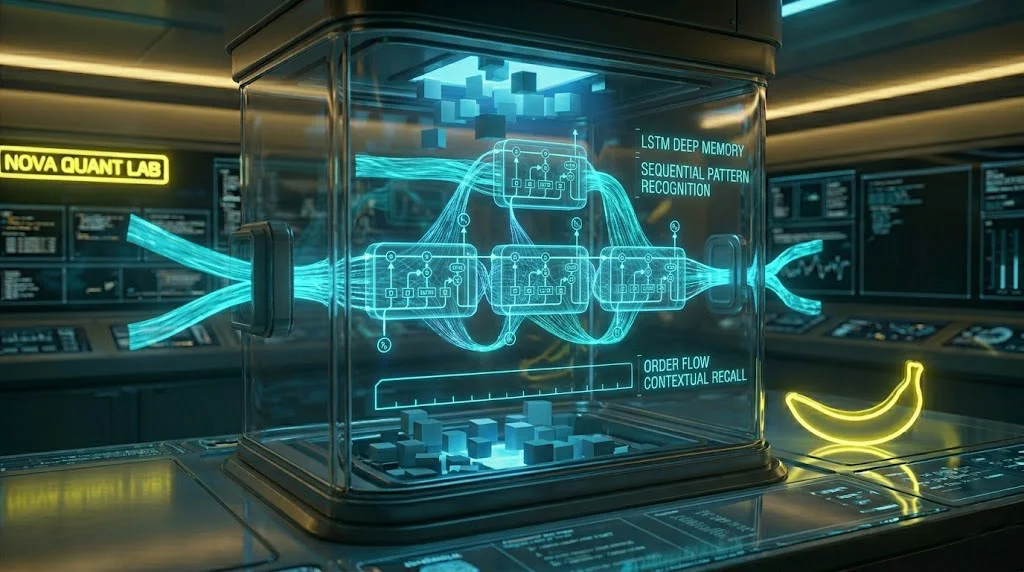

The River of Time: Deep Learning and Sequential Pattern Recognition with LSTMs

Welcome back to Nova Quant Lab. In our journey through Season 3, we have successfully elevated our quantitative infrastructure from deterministic classical statistics to the probabilistic realm of Machine Learning. In Posts 10, 11, and 12, we engineered real-time features, trained a LightGBM classification engine, and forged it in the crucible of Purged K-Fold Cross-Validation.…

-

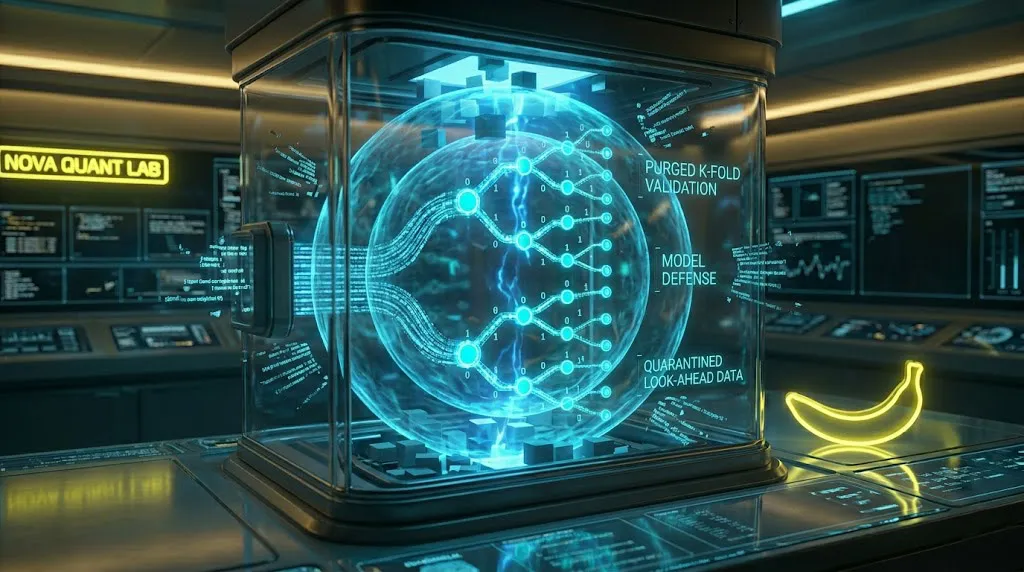

The Crucible of Truth: Purged K-Fold Cross-Validation in Financial Machine Learning

Welcome back to Nova Quant Lab. If you have successfully implemented the architecture from Post 11, you are currently staring at a Jupyter Notebook that is likely displaying a phenomenal result. Your LightGBM model, trained on your engineered Order Book Imbalance (OBI) features, might be showing a Test Accuracy of 85%, 90%, or even 95%.…

-

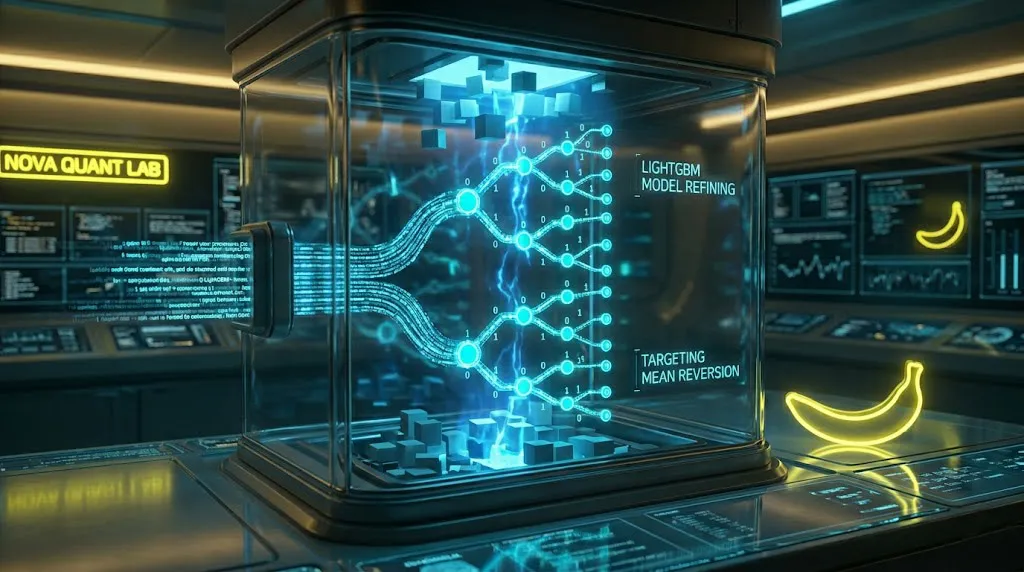

The Prediction Engine: Training and Tuning LightGBM for High-Frequency Arbitrage

Welcome back to Nova Quant Lab. In our previous session (Post 10), we built the Data Refinery. We wrote the high-performance Python code required to ingest raw, chaotic WebSocket order book data and transform it into structured, mathematically stationary features like the Depth-Weighted Order Book Imbalance (OBI) and the Micro-Price Momentum. We successfully converted market…

-

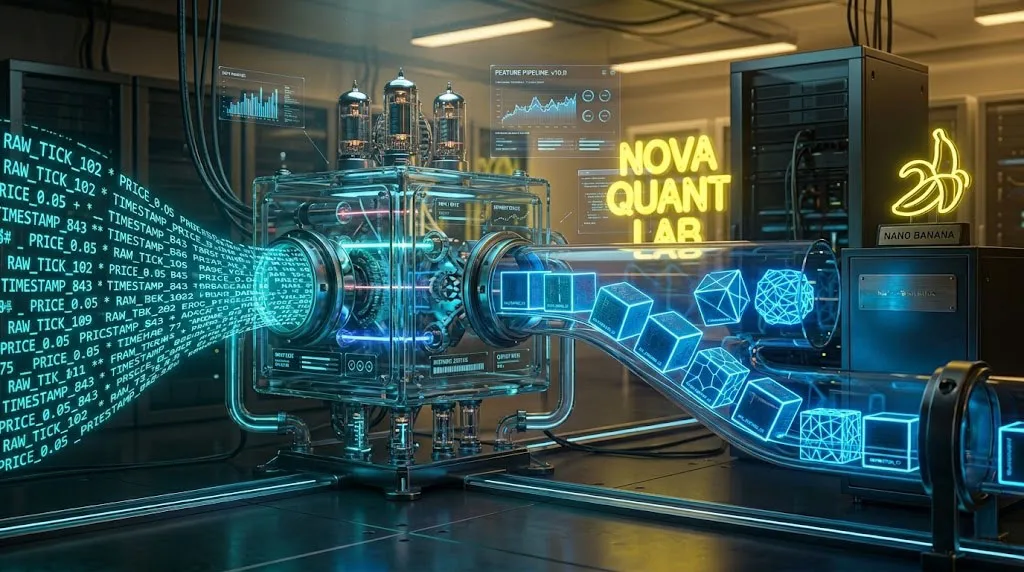

The Data Alchemist: Real-Time Feature Engineering from Order Book Data in Python

Welcome back to Nova Quant Lab. In our previous session, we laid the theoretical groundwork for Season 3. We discussed the transition from classical, linear statistical models to the non-linear, hyper-dimensional realm of Machine Learning (ML). We introduced the concept of the Order Book Imbalance (OBI) and established that feeding raw price data into an…

-

The New Frontier: Integrating Machine Learning into Quantitative Arbitrage

Welcome back to Nova Quant Lab, and welcome to the highly anticipated Season 3. If you have survived the crucible of Season 2, you are no longer a retail trader. You are the architect of a robust, automated quantitative infrastructure. You have built a Python-based execution engine capable of atomic concurrency, you have deployed it…

-

The Ghost in the Data: Mastering Statistical Arbitrage and Cointegration in Python

Welcome back to Nova Quant Lab. We have traveled a vast distance in Season 2. We have moved from the raw infrastructure of 24GB cloud servers to the atomic execution of multi-leg orders across global exchanges. In Post 7, we explored the world of multi-asset portfolios and deterministic basis trading. But now, we are about…

-

Diversified Dominance: Multi-Asset Portfolio Management and Basis Trading Strategies

Welcome back to Nova Quant Lab. In our journey through Season 2, we have transitioned from the psychological turmoil of manual trading to the cold, calculated precision of quantitative infrastructure. We have built the eyes, the muscles, and the brain of our machine. In Post 6, we learned how to interrogate our logs and measure…

-

Beyond the Build: Performance Analytics and Multi-Exchange Scaling for Delta-Neutral Bots

Welcome back to Nova Quant Lab. We have officially crossed the technical rubicon. In our previous installments of Season 2, we moved with surgical precision to build the “High-Frequency Arbitrage Infrastructure.” We engineered the eyes to observe the market (Asynchronous Ingestion), the muscles to act (Execution Engine), the brain to strategize (Signal Orchestrator), and the…

-

The Fortress of Yield: Production Deployment and Kernel Optimization for High-Performance Quant Trading

Welcome back to Nova Quant Lab. We have arrived at the final technical milestone of our Season 2 infrastructure series. If you have been following our journey closely, you have successfully engineered a sophisticated piece of quantitative machinery. You have built the eyes to observe the market (Asynchronous Ingestion), the muscles to act (Execution Engine),…

-

The Brain of the Machine: Designing a High-Precision Net-Yield Signal Orchestrator in Python

Welcome back to Nova Quant Lab. We have reached the pivotal milestone in our Season 2 journey. Over the last few weeks, we have successfully engineered the sensory organs (the Asynchronous Data Ingestion Module) and the muscular system (the Concurrent Execution Engine) of our algorithmic trading bot. Our server is now flooded with real-time, Level…